TL;DR:

Section 179 and Bonus Depreciation (Section 168(k)) offer powerful tax-saving opportunities for businesses investing in equipment. For 2026, Section 179 allows up to $2.56M in deductions on qualifying purchases placed in service by December 31, 2026, and Bonus Depreciation remains at 100%. These provisions apply to new and used equipment, certain real property improvements, and more—but they come with considerations like future tax impact and balance sheet effects. Always consult a tax advisor before leveraging these strategies.

Over the years many companies have saved on their taxes by taking advantage of Section 179 and Section 168(k) of the IRS Tax Code. Herein we’ve provided some information about the opportunity for tax savings, the changes, and things to consider in order to take advantage of the tax benefits.

What is Section 179?

Section 179 allows eligible businesses to deduct the full purchase price of qualifying equipment in the year it was put into service. This results in a larger initial expense deduction than using a standard depreciation method, thereby reducing the company's tax burden.

The eligible equipment can be financed or paid for with cash. In order to take advantage of the accelerated depreciation the tax code requires that the equipment be put into service before December 31 of the applicable tax year. During the past couple of years we've seen extended lead times for equipment, so it's important to take delivery timing into consideration if you intend to take advantage of these tax breaks.

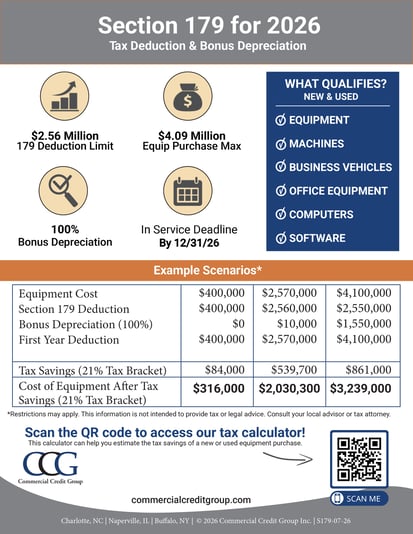

While there are some limitations on the amounts and types of equipment, the allowances are sufficient for many small and medium-sized companies to realize substantial savings. These provisions of the Tax Code have long existed, but the 2018 tax changes were noteworthy. These include the ability to take a deduction for the purchase of used equipment (as long as the equipment is “new to you”) and an increase in the limitation amounts. For tax year 2026, the Section 179 deduction limit is $2,560,000 (up from $2,500,000 in 2025).

What are the Section 179 Limits?

- Maximum amount that can be deducted is $2,560,000

- Maximum amount of equipment that can be purchased (and take the full deduction) is $4,090,000

- Equipment must be placed into service no later than December 31, 2026

If total equipment purchases exceed $4,090,000, the Section 179 deduction decreases dollar for dollar, reaching zero once $6,650,000 of equipment is purchased &/or financed. However, bonus depreciation has no limit, as noted below.

What is Bonus Depreciation?

Section 168(k) allows for bonus depreciation on eligible equipment and property, thereby enabling accelerated depreciation and a reduced tax burden, similar to Section 179. A company can take both Section 179 and Bonus Depreciation allowances, but Section 179 must be applied first, and any amount over the $2,560,000 limit to Section 179 may then be taken in bonus depreciation.

Effective on 7/4/25, with the signing of the "Big Beautiful Bill" in law, bonus depreciation was restored to 100%. It had previously been set to reduce to 40% for tax year 2025, as noted in the 2018 Tax Cuts and Job Act (TCJA).

One thing to note is that a company must be profitable in order to take the Section 179 deduction; it cannot be applied to create a net loss for the business. However, there is currently no business income limitation for bonus depreciation, so a business could take a net loss by taking advantage of bonus depreciation.

To record bonus depreciation, businesses should use IRS Form 4562.

Normal depreciation

Because the bonus depreciation allowance has been restored to 100%, if a company uses bonus depreciation to reduce the book value of an asset to $0, normal depreciation no longer applies.

What is Considered Eligible Equipment?

Eligible equipment includes heavy equipment and machinery, office and computer equipment, off-the-shelf software, and certain business-use vehicles (check with your legal or tax advisor to determine if your purchases qualify).

In short, if the equipment qualifies as a depreciable asset under Section 168 and is acquired for use in the operation of the business, it should be allowed.

The Tax Cuts and Jobs Act (TCJA) expanded the definition of "qualified real property" to include improvements (Qualified Improvement Property - QIP) to nonresidential real estate such as roofs; HVAC systems; fire protection, alarm and security systems. The CARES Act of 2020 further modified the rules for the treatment of QIP, classifying it as 15-year property rather than 39-year property, and no longer subjecting it to the $2 million a year limit for Bonus Depreciation.

What are the Concerns about Using Section 179 and Bonus Depreciation?

Before you take Section 179 and/or bonus depreciation deductions, consult with your tax or legal advisor. While it’s true that the deductions effectively reduce your tax burden for the year in which the equipment was purchased, you may also give up future years’ depreciation, thereby impacting subsequent years’ tax burdens as well.

Additionally, accelerated depreciation of an asset results in a lower book value for that asset, which will affect the debt-to-worth ratio of your balance sheet (if you rely on tax returns or tax values in preparing your financial statements). While this may not have a significant impact on your business, it could affect your ability to borrow money for future purchases. And if you decide to sell the asset, specifically at a price higher than the current book value, you could pay taxes on the gains from that sale.

Evaluating the short and long-term effects of your purchase decisions and tax strategies is important to running your business. Your tax advisor can help you evaluate the effects of these tax strategies, so you can make the most informed decisions.

Buying equipment before the end of the year?

If you need equipment before the end of the year to qualify for Section 179 or Bonus Depreciation, CCG can help. Contact us today or learn more about our financial services.

Want to know how much you can save with Section 179? Estimate your savings with the "Section 179 Calculator":

Resources:

To learn more about the history of Section 179, read this report from the Congressional Research Service.

To learn more about Depreciation, the IRS has published a list of Depreciation FAQs.

Journal of Accountancy - https://www.journalofaccountancy.com/news/2020/oct/2021-irs-tax-tables-inflation-adjustments.html

https://www.bipc.com/one-big,-beautiful-bill-.-.-.-simplified

Subscribe to Our Blog

Want to know when our blog has been updated with new posts?

Complete our short form and we’ll make sure you are informed.

Fill out our short form to subscribe